FX Daily Strategy: Europe, April 24th

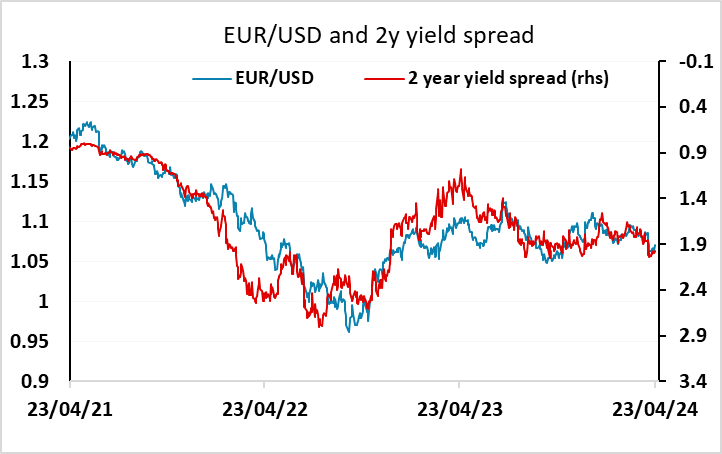

IFO needs to beat consensus to justify EUR/USD strength

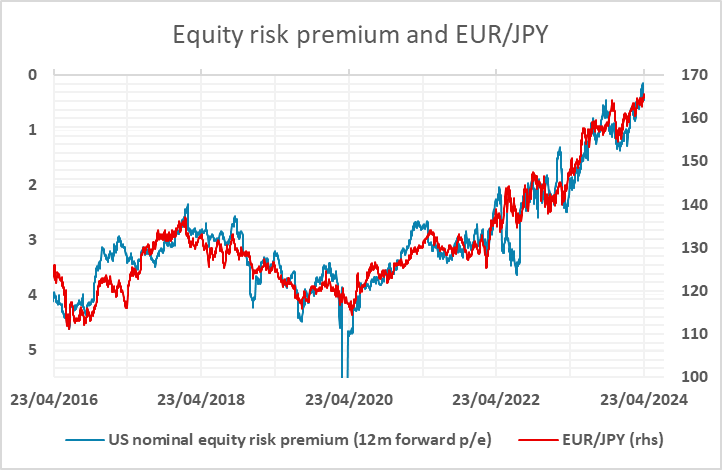

EUR/JPY move to new highs may be temporary

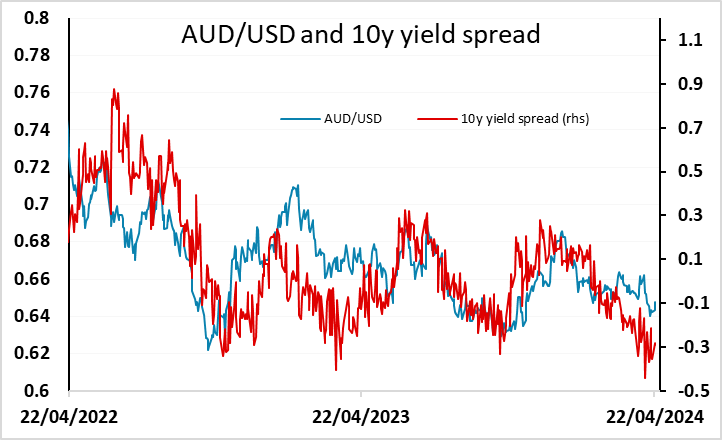

Hotter CPI to Support Aussie in a Short Run

IFO needs to beat consensus to justify EUR/USD strength

EUR/JPY move to new highs may be temporary

Hotter CPI to Support Aussie in a Short Run

Wednesday’s calendar is relatively quiet, but there will probably be more interest than usual in the German IFO survey after the improvement in the PMI surveys on Tuesday. The IFO business climate index has generally mirrored the composite PMI index in the last year, so while the market consensus is for a rise, the PMI data suggests the rise may be a little larger than the published consensus suggests. While the consensus is 88.9, we could see something close to 90 if the IFO survey follows the PMI. Something better than the published consensus will be priced into the market after the PMI data, but probably something gin the low 89s rather than anything close to 90.

For EUR/USD, a strong number may be required to maintain the gain above 1.07 seen on Tuesday. This was due more to the weakness of the US PMI survey than the strength of the European data, but even though EUR/USD rose, the rise was not really supported by any move in yield spreads, with European yields dropping back with the US. At this point, the market isn’t ready to believe that the European economy is about to outperform the US, so a strong IFO survey looks necessary just to sustain Tuesday’s modest EUR gains.

The EUR (and GBP) also made gains against the JPY on Tuesday as a consequence of the weaker US numbers and the stronger numbers in Europe. Of course, the Japanese PMI data was also strong, but no-one pays attention to that. The strength of EUR/JPY typically reflects positive global risk appetite rather than any specific economics, and the equity market gains after the US data consequently helped EUR/JPY to break above 165 hitting new 16 year highs at 165.75. But as we have noted before, EUR/JPY doesn’t typically follow equity indices, but rather reflects moves in the equity risk premium. Equity gains based on lower yields consequently don’t typically have a sustained positive impact. However, if anything EUR/JPY has been lagging behind the decline in equity risk premia of late, so at this stage we wouldn’t expect a significant turn lower in EUR/JPY unless the BoJ decide that enough s enough and it’s time to intervene. We doubt this will be the case unless USD/JPY also recovers and makes new highs above 155.

Before the IFO survey we have Australian CPI data which could impact market expectations for RBA policy. The AUD also benefited from the weaker US data on Tuesday, and could make further gains if the CPI data is strong enough to eliminate market expectations of RBA easing this year. As it stands, the market is pricing 17bps of easing by the end of the year. Q1 CPI is expected to drop to 3.4% y/y, and that would maintain these expectations. A smaller drop looks necessary to allow AUD/USD to test 0.65 as yield spreads still suggest there is scope for more USD strength.

The latest Australian Q1 CPI came in hotter than expected with q/q at +1.0%, above expectation of 0.8% and y/y at +3.6%, also above expectation of 3.4%. However, the data still signals a continue moderation of CPI as y/y dropped to 3.6% from 4.1% and should not be read as a turn for RBA's rate path. Still, it pushes away the idea of an early easing from the RBA for inflation has not reached its target yet and may reduce any speculative shorts in the Aussie in a short run.