FX Daily Strategy: N America, May 3rd

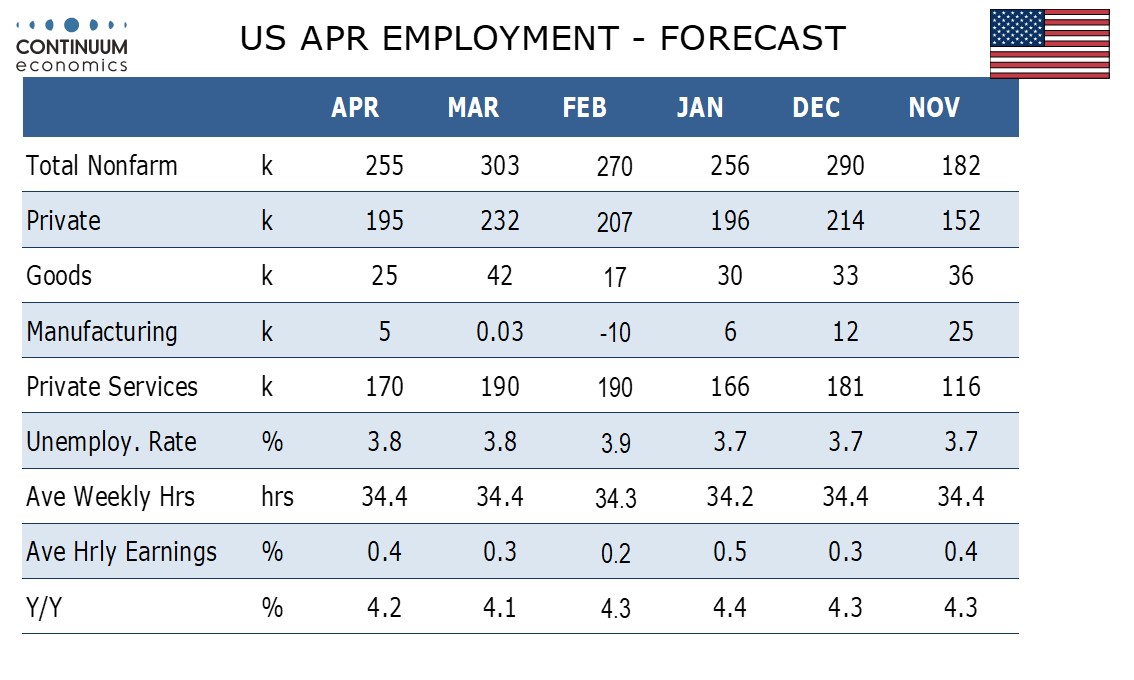

USD to get support from US employment report

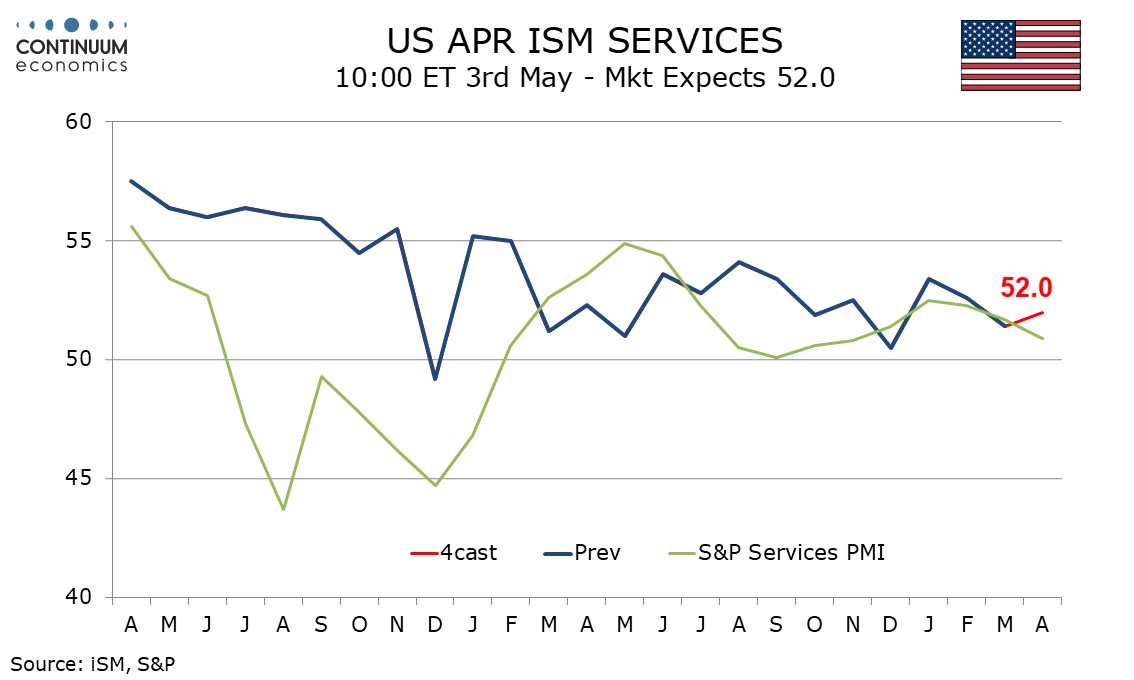

ISM services should be neutral, but some downside risks

JPY strength to continue long run, but some consolidation may be seen near term

NOK has upside scope despite recent weakness with Norges Bank likely to remain steady

USD to get support from US employment report

ISM services should be neutral, but some downside risks

JPY strength to continue long run, but some consolidation may be seen near term

NOK has upside scope despite recent weakness with Norges Bank likely to remain steady

Friday will be dominated by the US employment report, although ISM services will play a supporting role. We expect a 255k increase in April’s non-farm payroll, still strong if the slowest since November, with a 195k increase in the private sector. We expect an unchanged unemployment rate of 3.8% and a slightly above trend 0.4% increase in average hourly earnings, lifted by a minimum wage hike in California. The main difference from the consensus is the 0.4% rise in earnings, with the market median at 0.3%. Our numbers look likely to be USD supportive.

We expect April’s ISM services index to see a modest increase to 52.0 from 51.6, pausing after two straight declines, leaving the index with no clear trend, and continuing to imply modest expansion. Our forecast is in line with market consensus, and should dispel some of the concerns related to the decline in the S&P services PMI. Coming after the employment report the data will be of lower importance, but weak data in line with the softer S&P number might reverse any impac of a strong employment number.

Thursday was a day of clear JPY strength. The BoJ intervention in Wellington looks to have convinced the market that they are serious and aren’t going to allow the JPY to stay at these exceptionally weak levels. The JPY strengthened through European and US sessions as well as gaining in direct response to the BoJ intervention in Asian time. The US session saw particular weakness in EUR/JPY and other JPY crosses, suggesting a widespread squeeze on JPY short positions. Nevertheless, both USD/JPY and EUR/JPY held above the lows seen in NZ time, and if these lows hold into Friday and there is no further BoJ action, we may see some consolidation in the new range of 153-158 going forward. Bigger picture, we still see scope for substantial JPY strength.

A somewhat more hawkish than expected statement from Norges Bank has sent the NOK higher. Norges bank said in their statement that “the data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged”. While they also noted that inflation has been a little lower than expected, they not that activity has been stronger and wage growth may turn out slightly higher than projected – considerations that suggests some upward pressure on inflation further out.

EUR/NOK initially around 4 figures on the announcement to 11.75. The market is still pricing in around a 73% chance of a rate cut by year end, but has reduced the probability from near 80%. Longer term yield spreads still suggests there is upside potential for the NOK based on recent correlations. Recent NOK weakness looks hard to explain, and the relatively low level and the carry advantage against the EUR suggests scope for EUR/NOK declines from here. NOK/SEK continues to look out of line as well, and given the historically very strong correlation with yield spreads, should have scope to challenge parity.